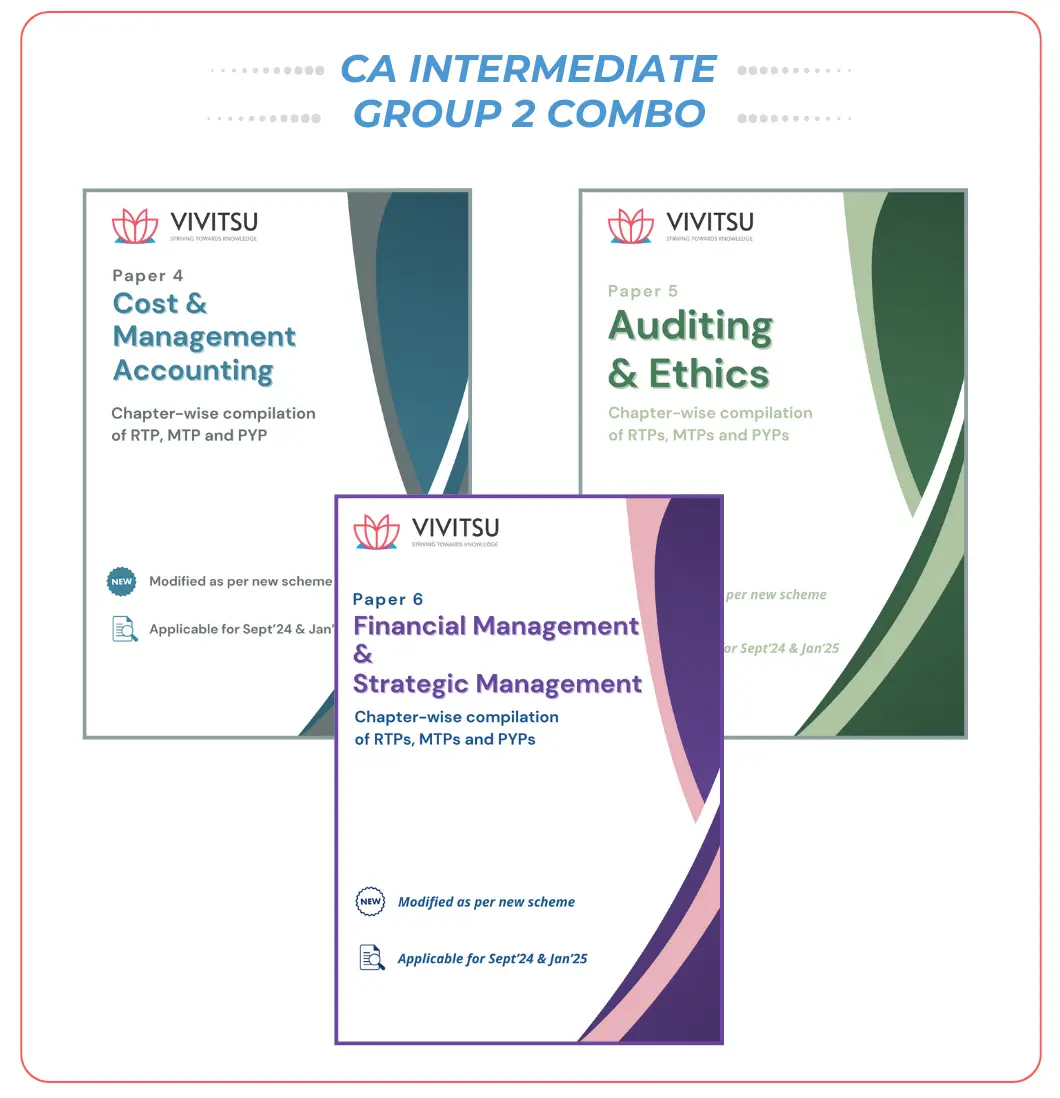

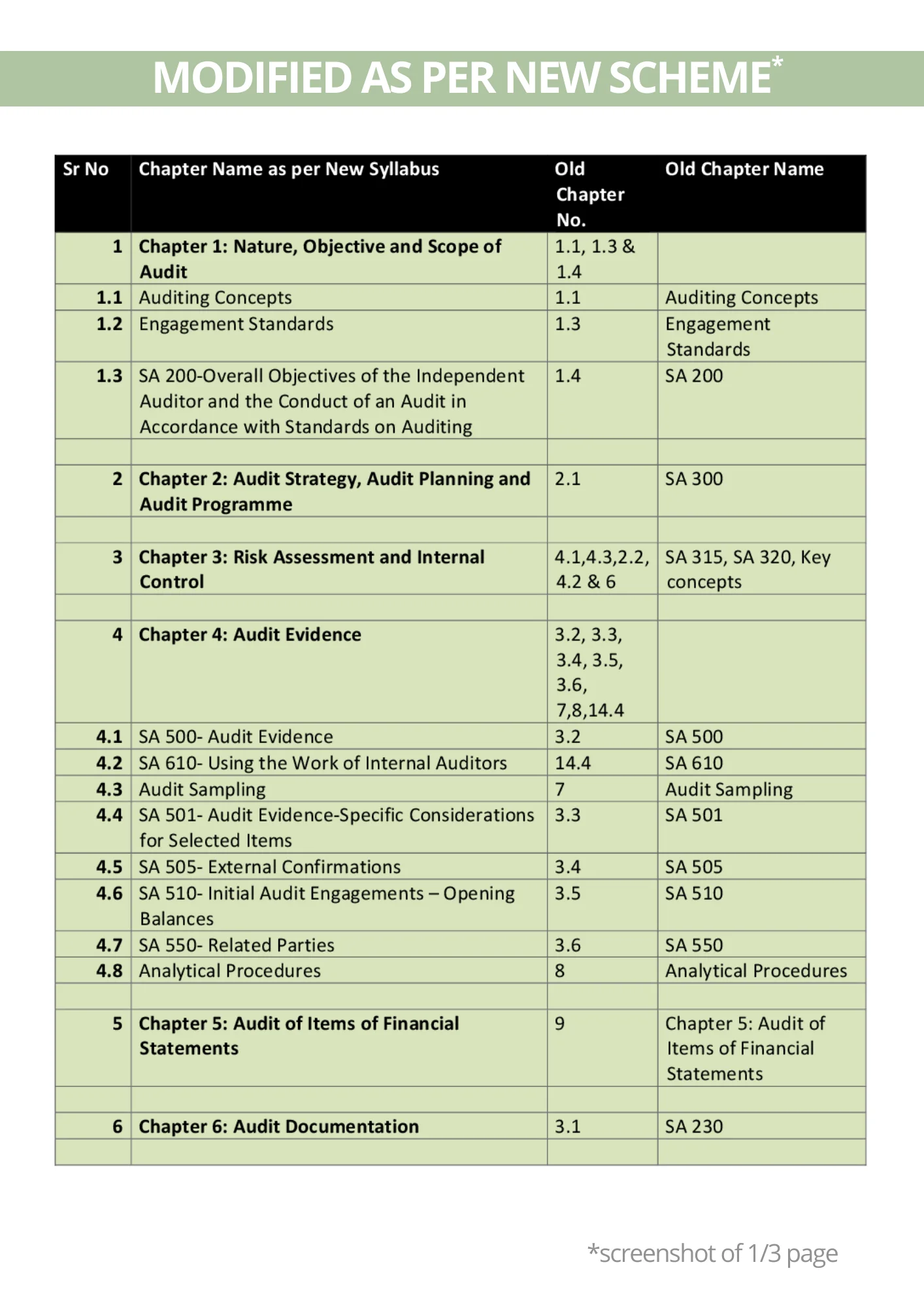

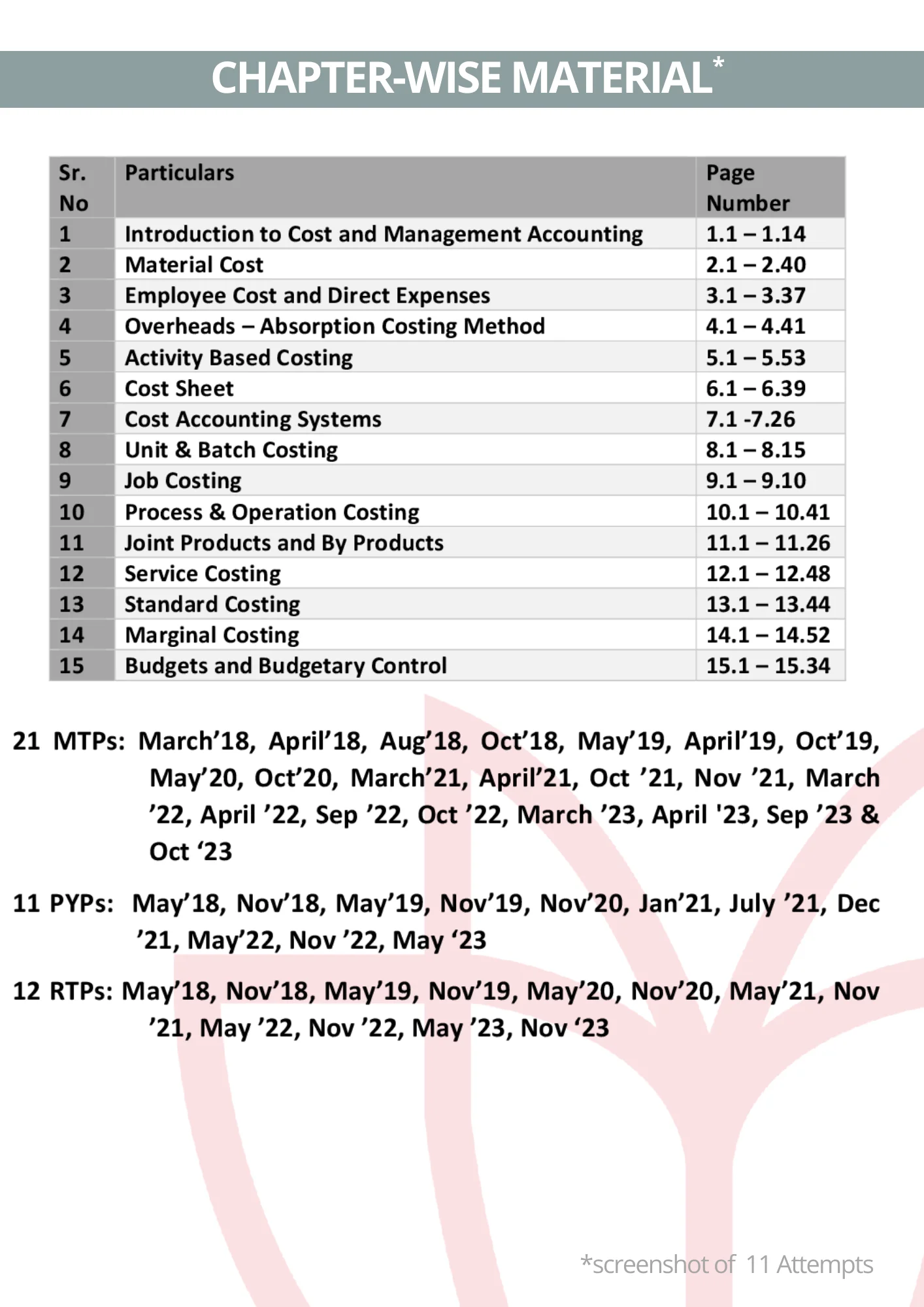

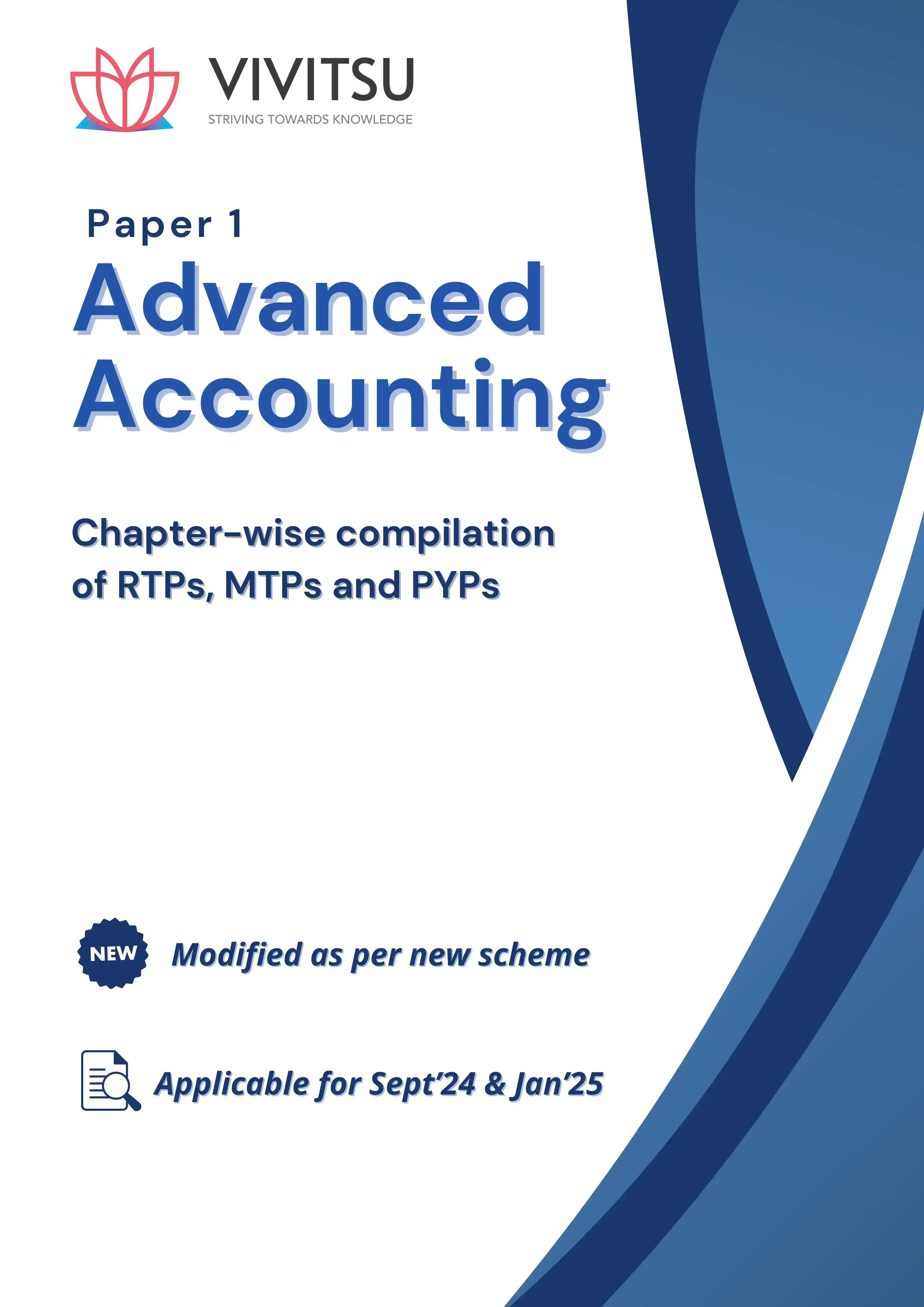

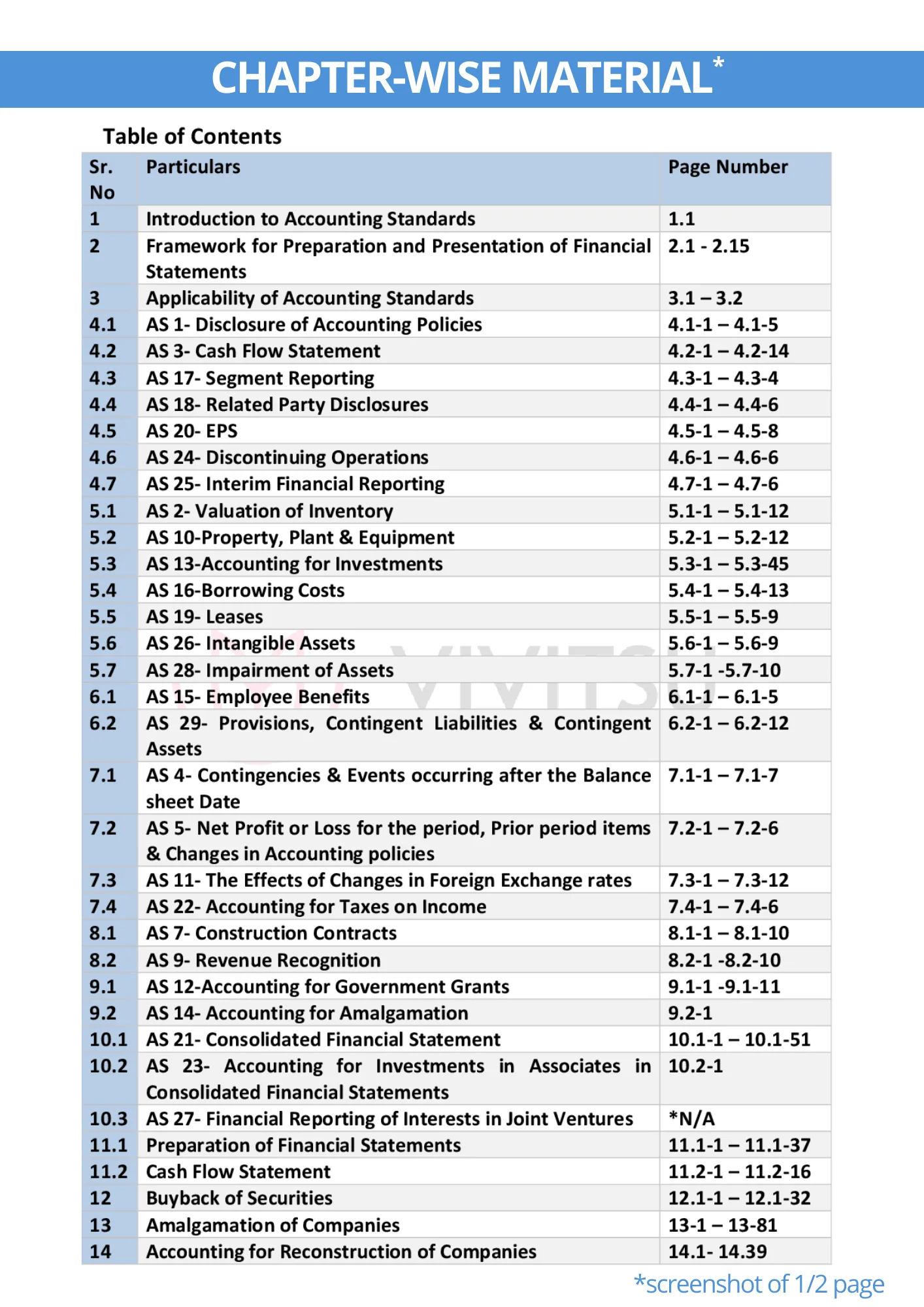

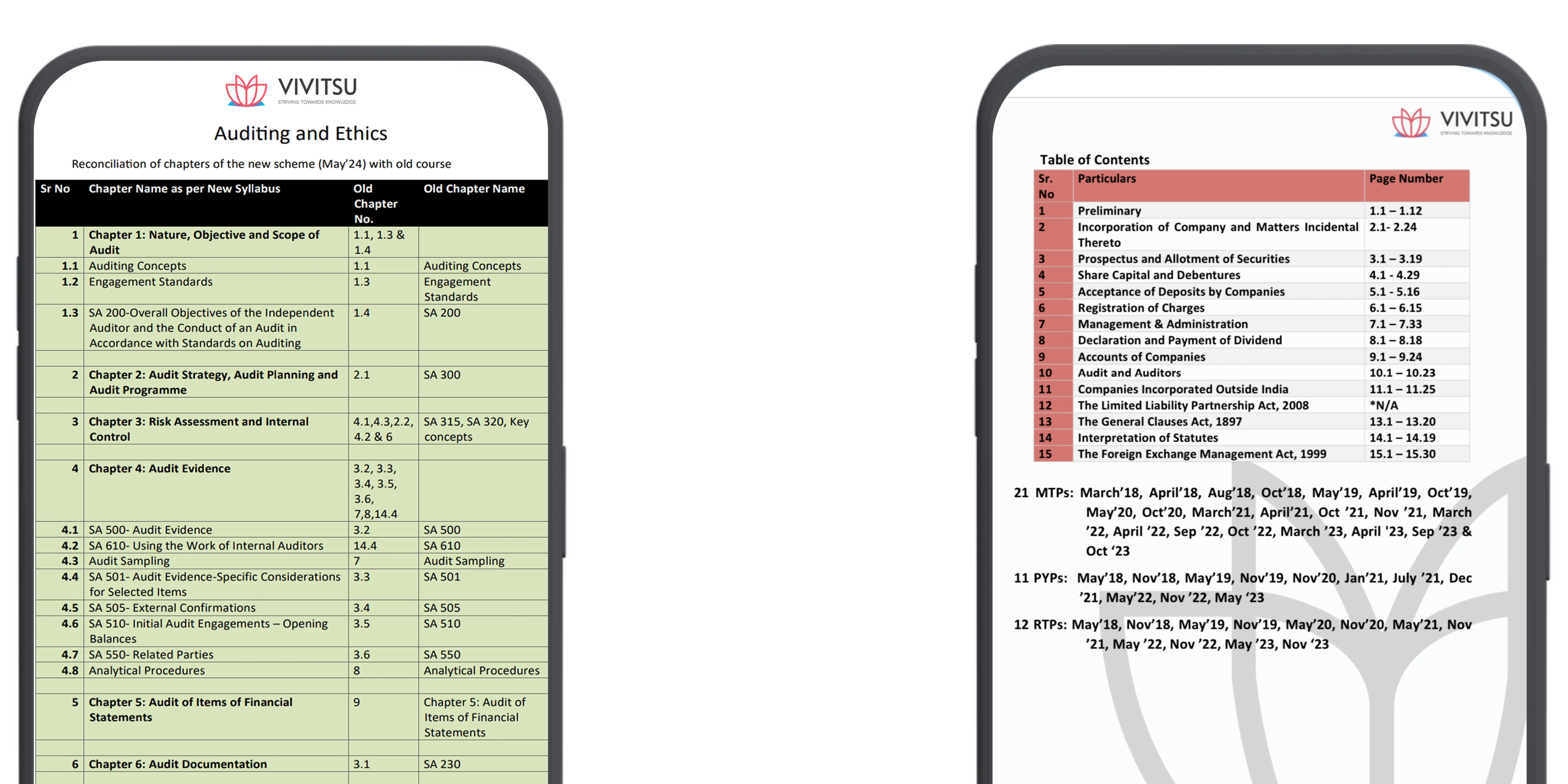

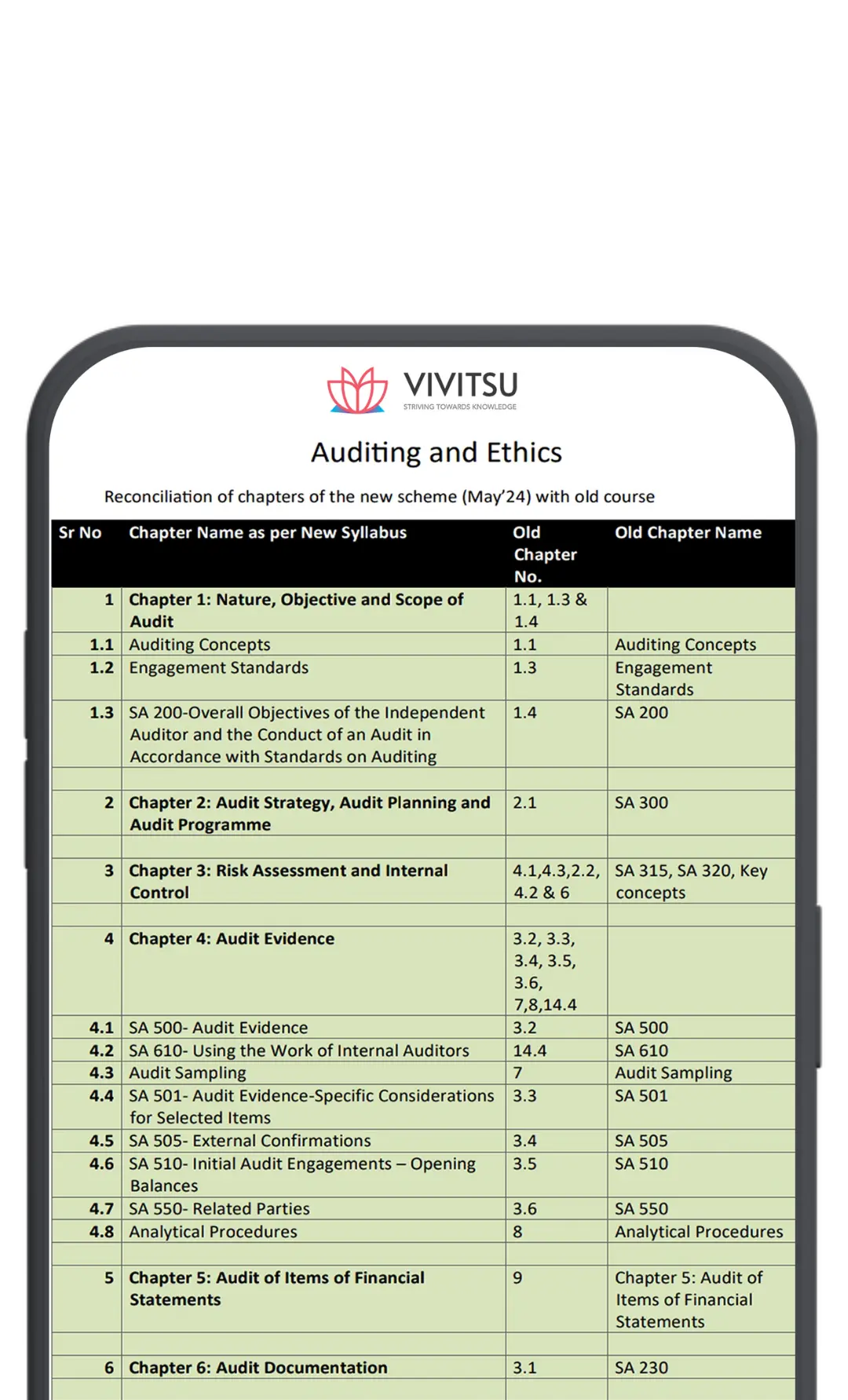

CA Intermediate Compilations for Sept'24/Jan'25

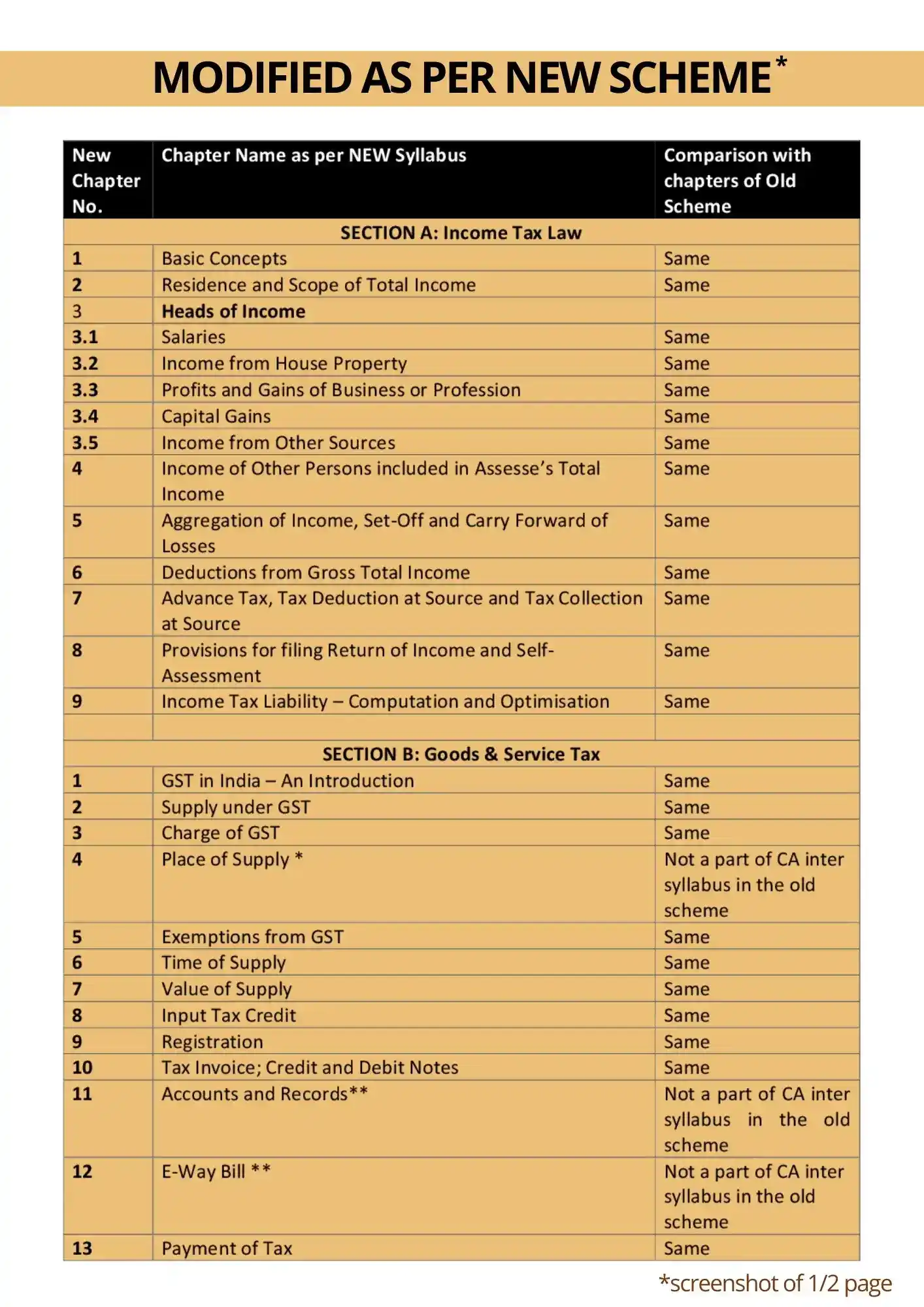

Applicable for New Scheme

20% + 30% off on combo "PDFCOMBO"

Flat 20% on individual subject "PDF20"

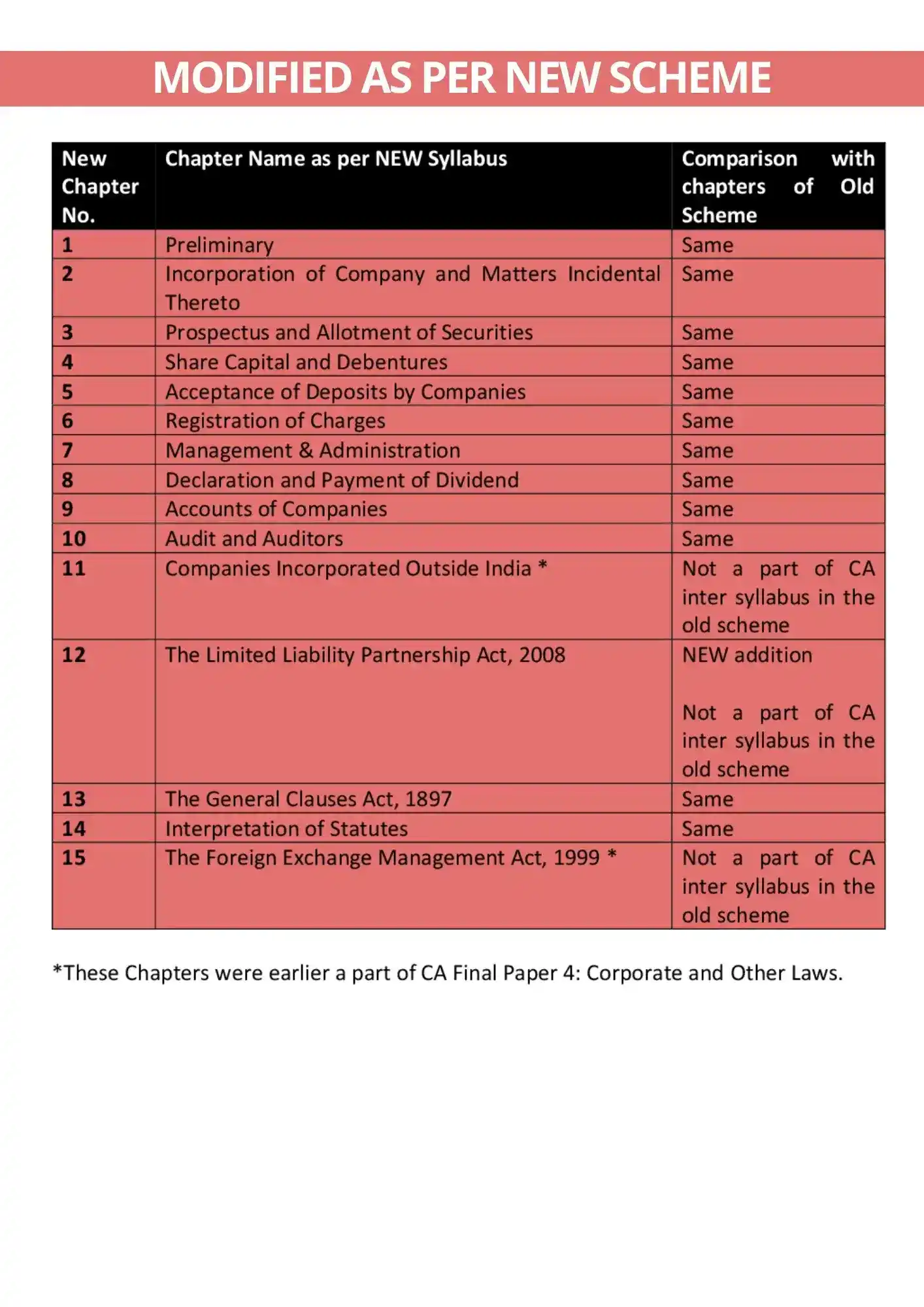

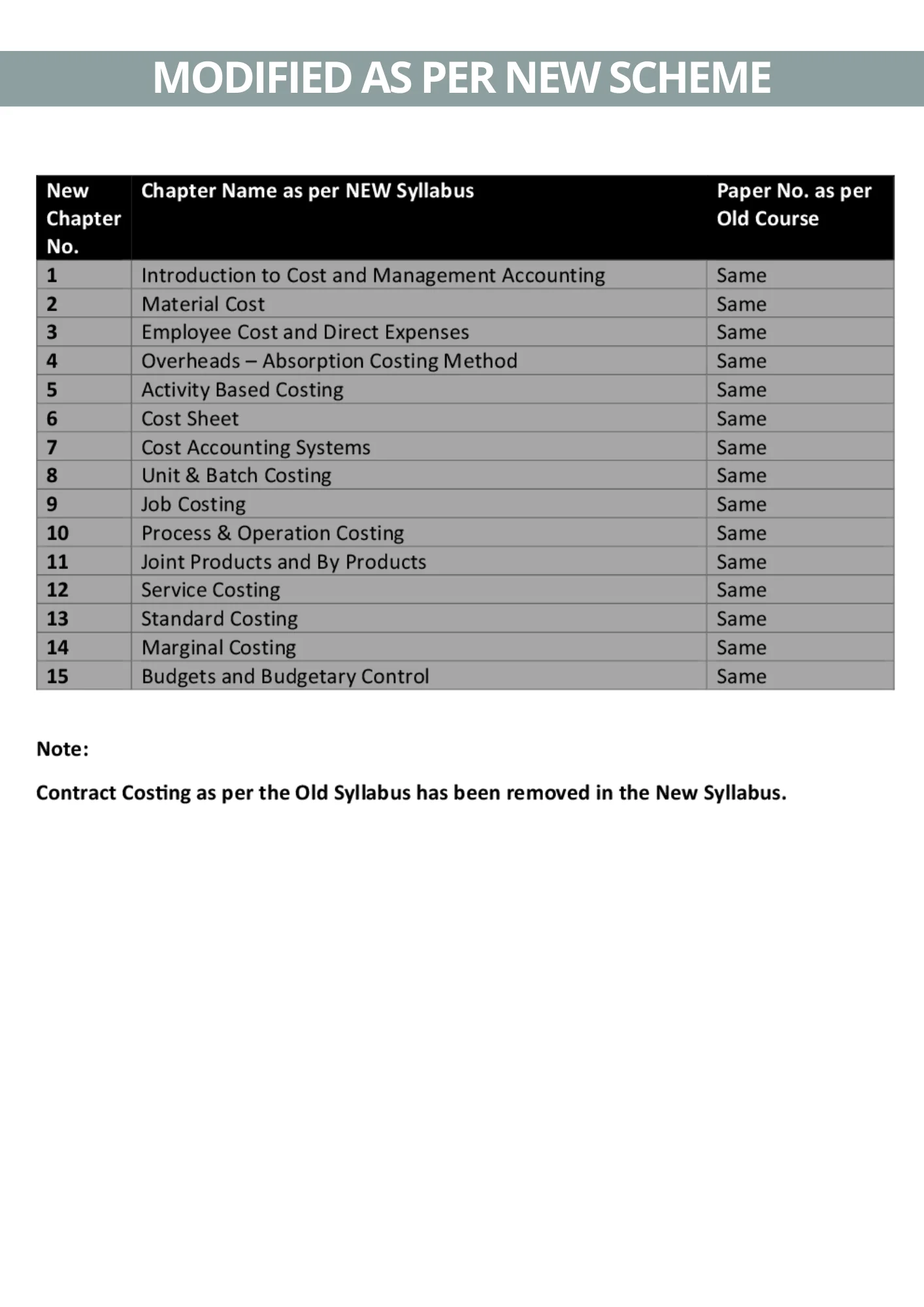

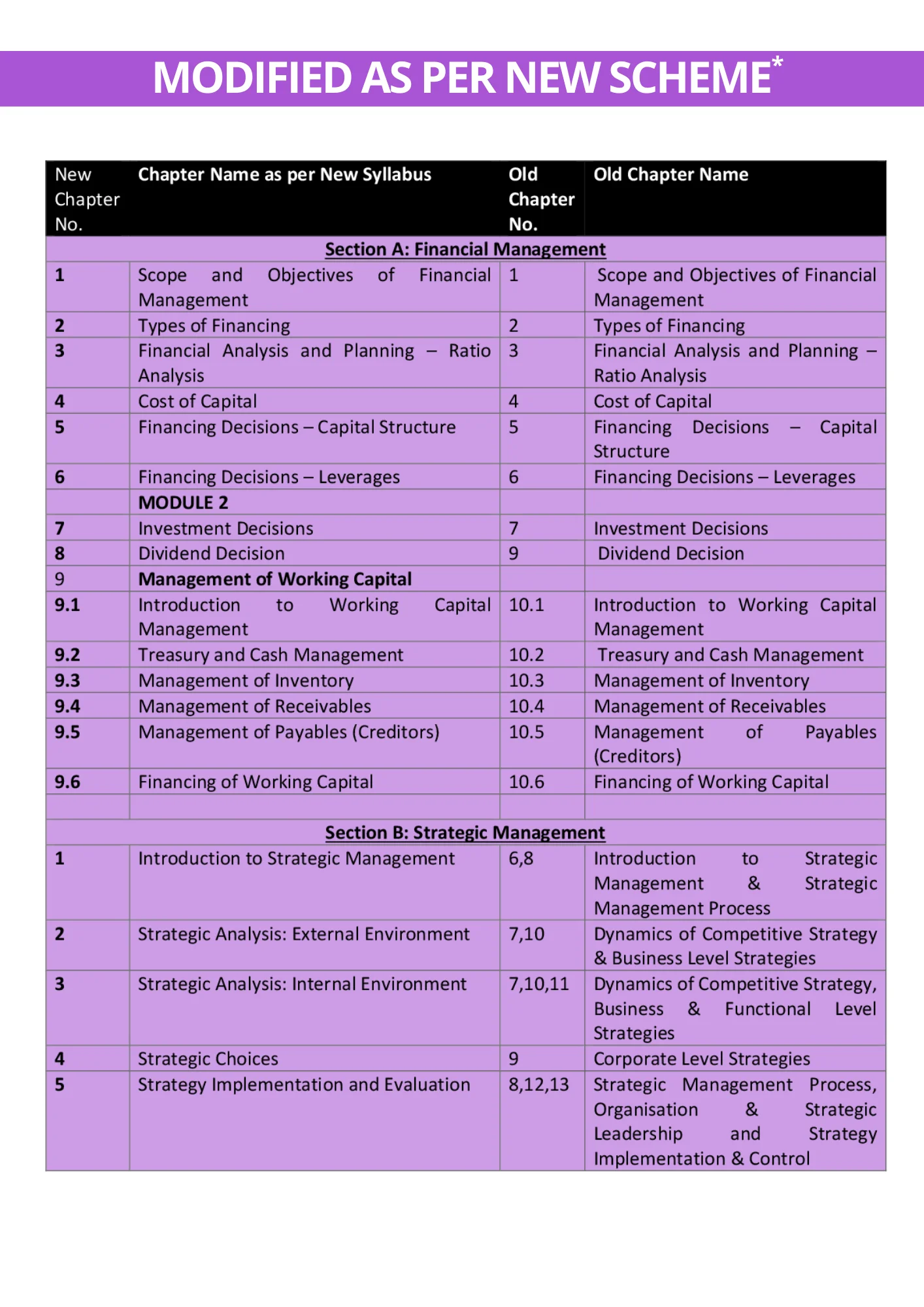

As per new scheme

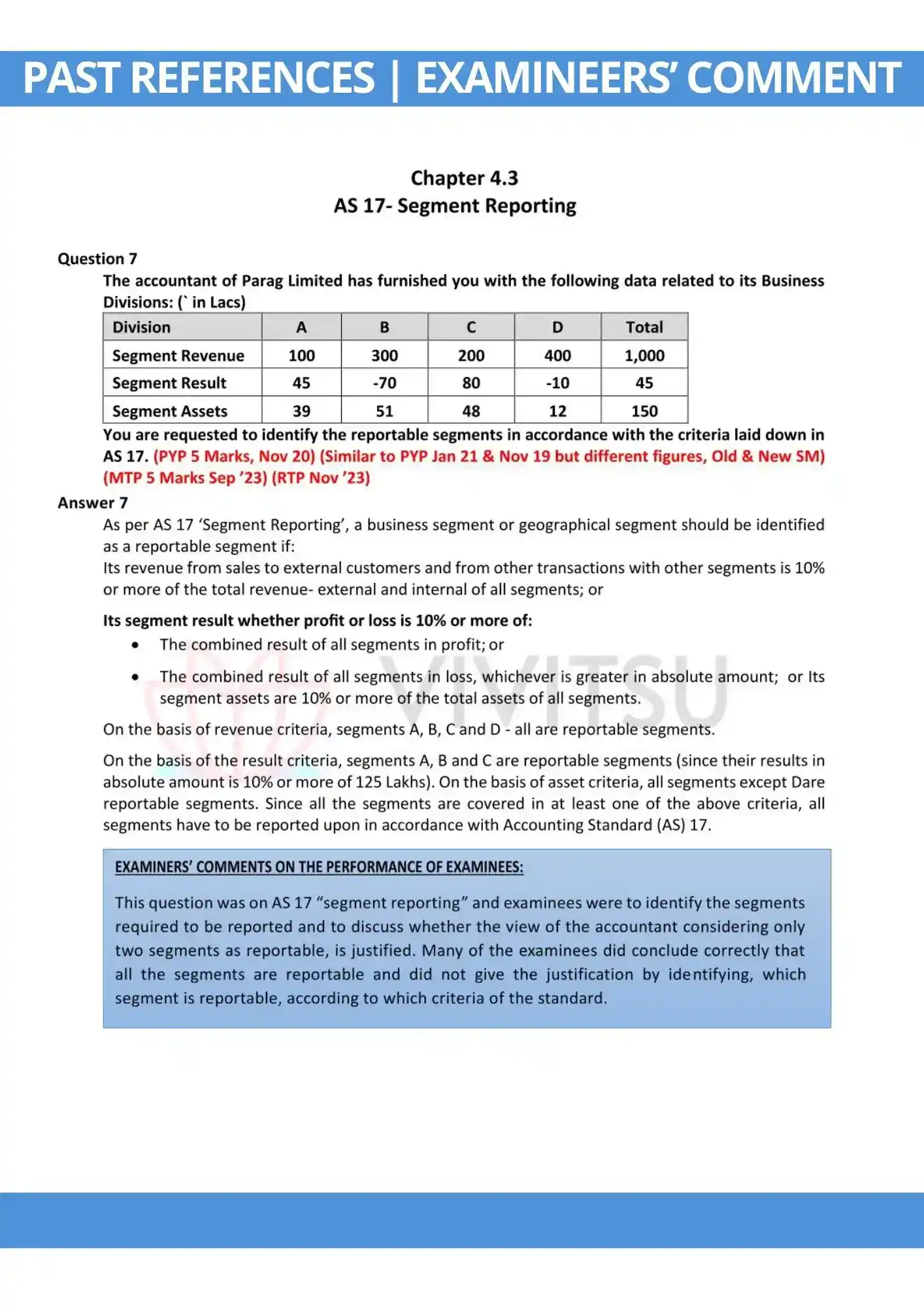

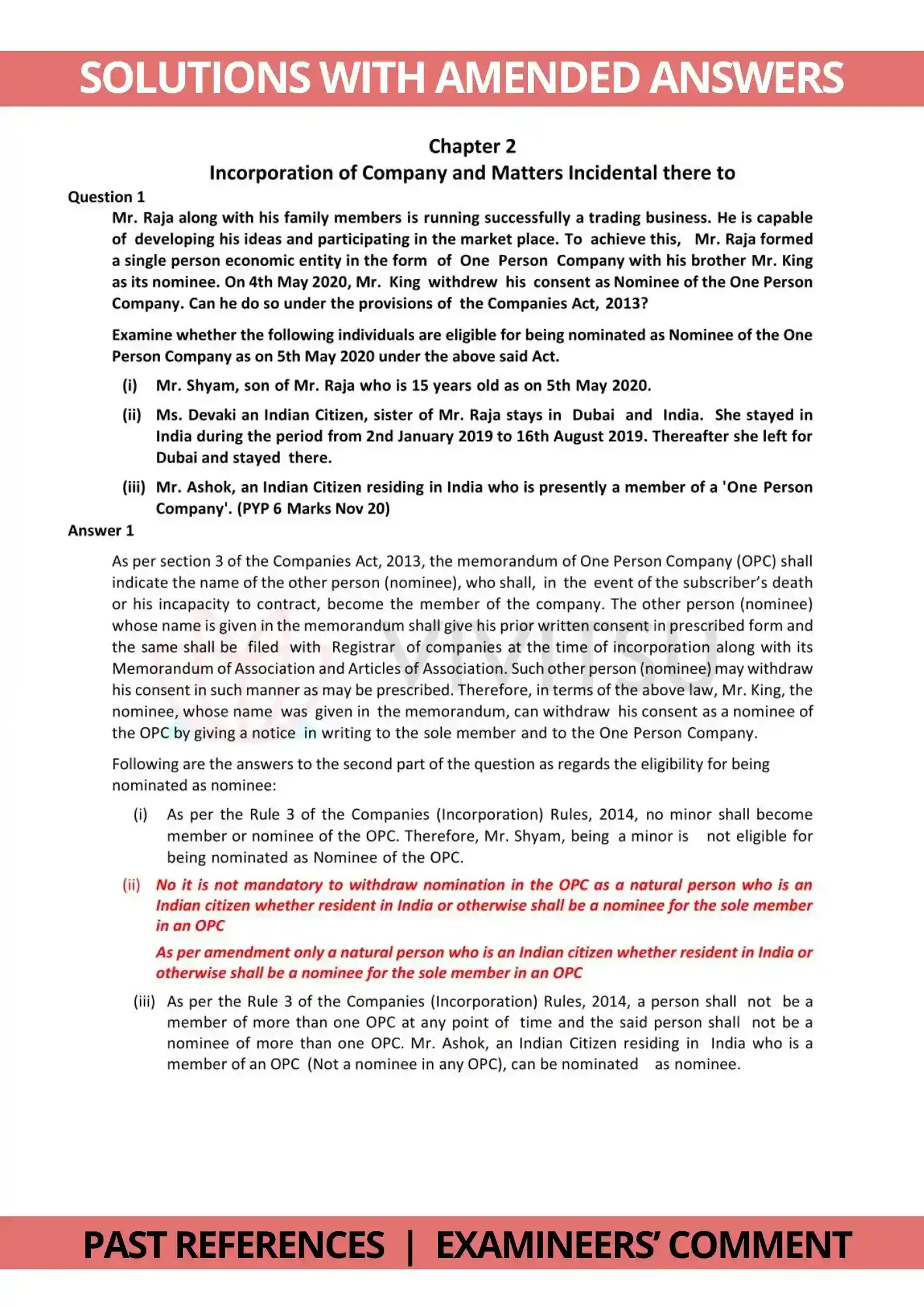

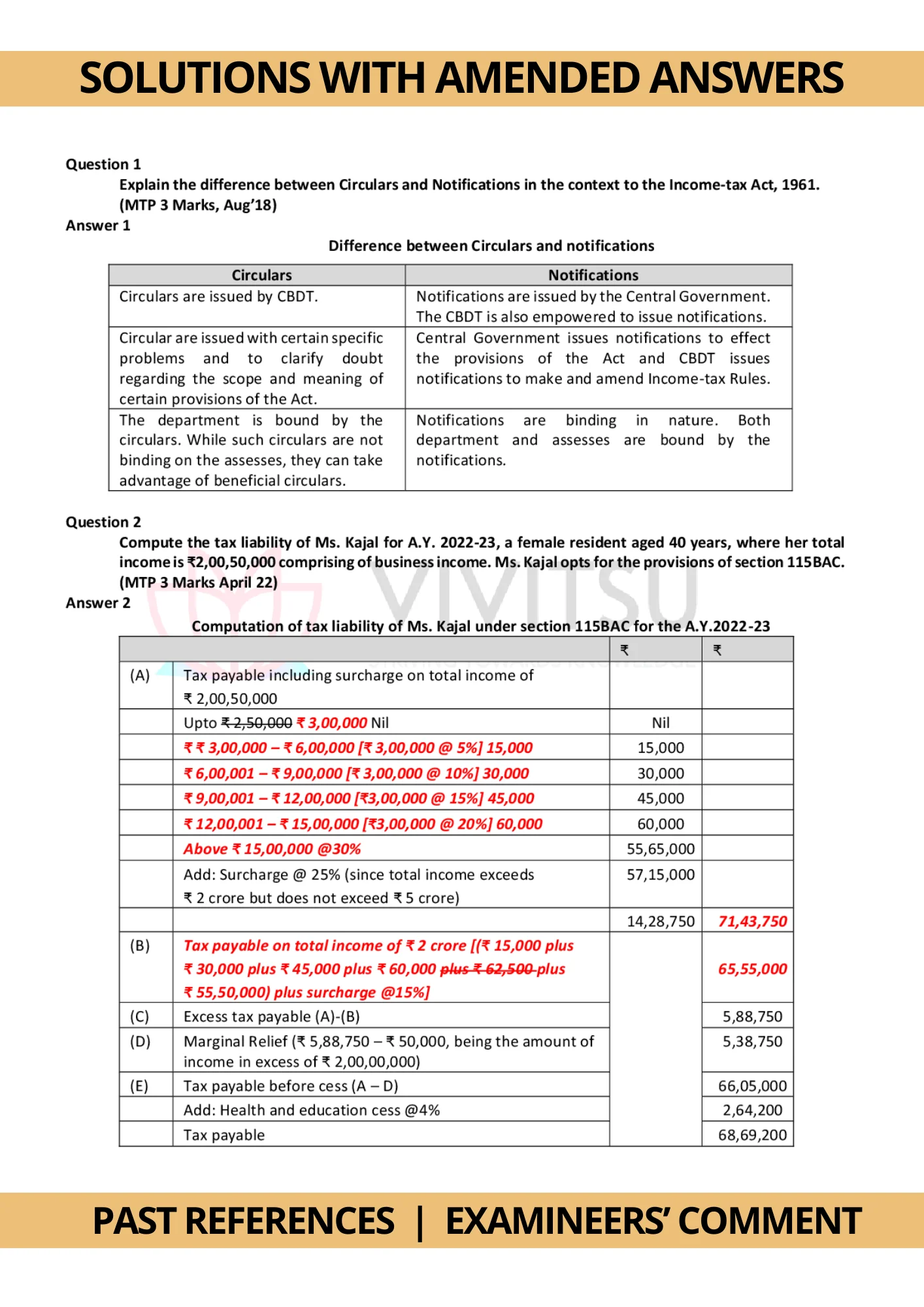

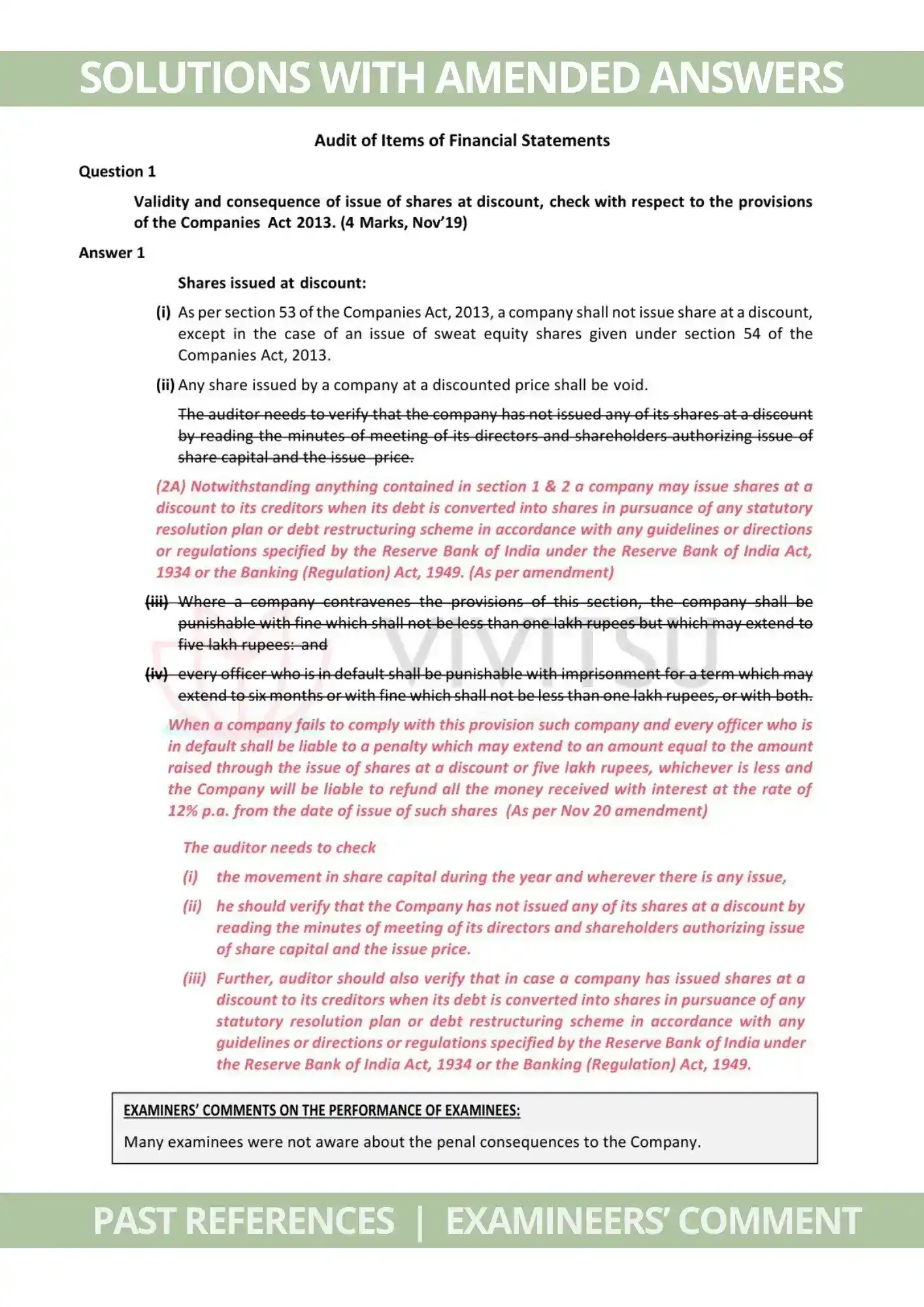

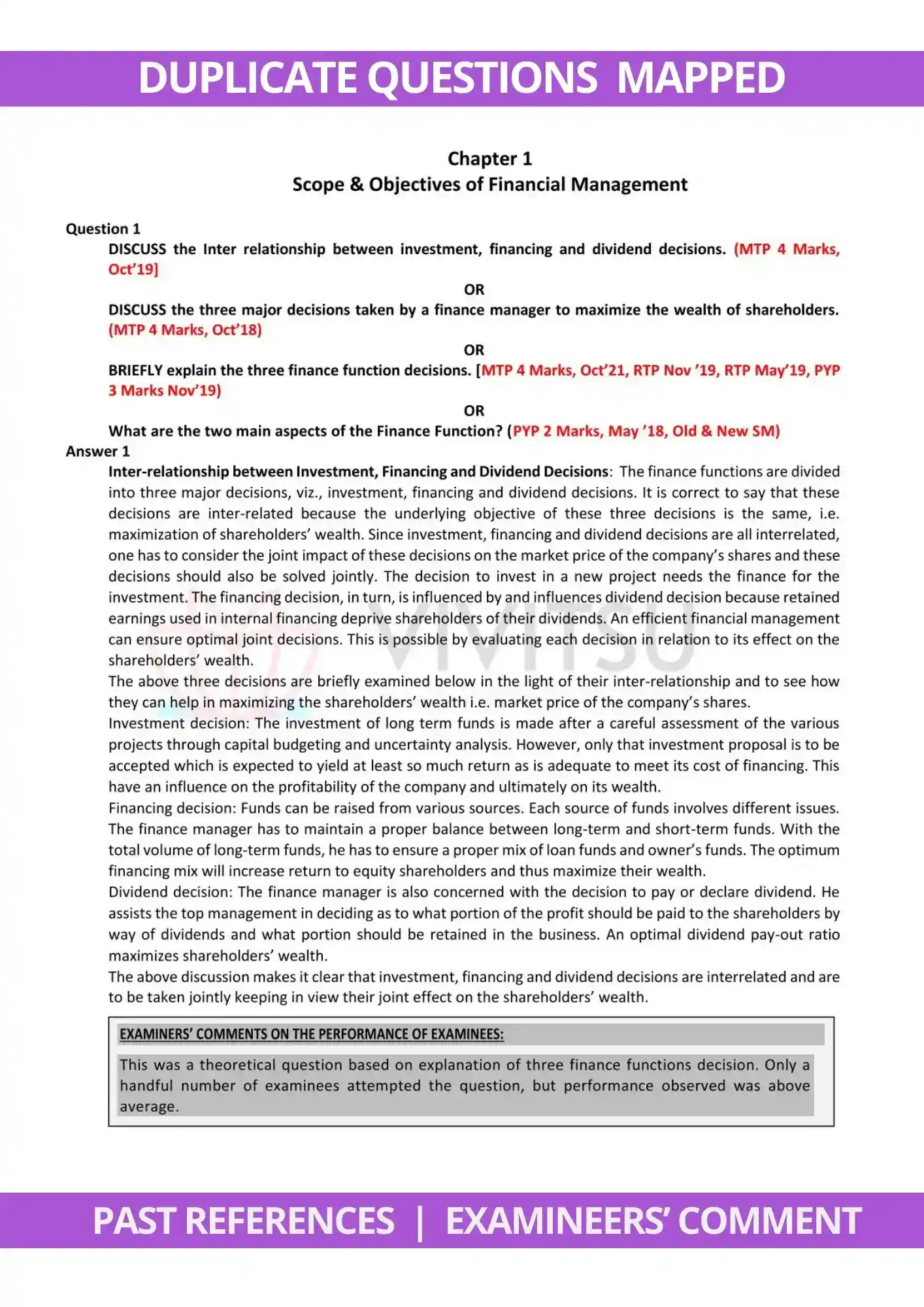

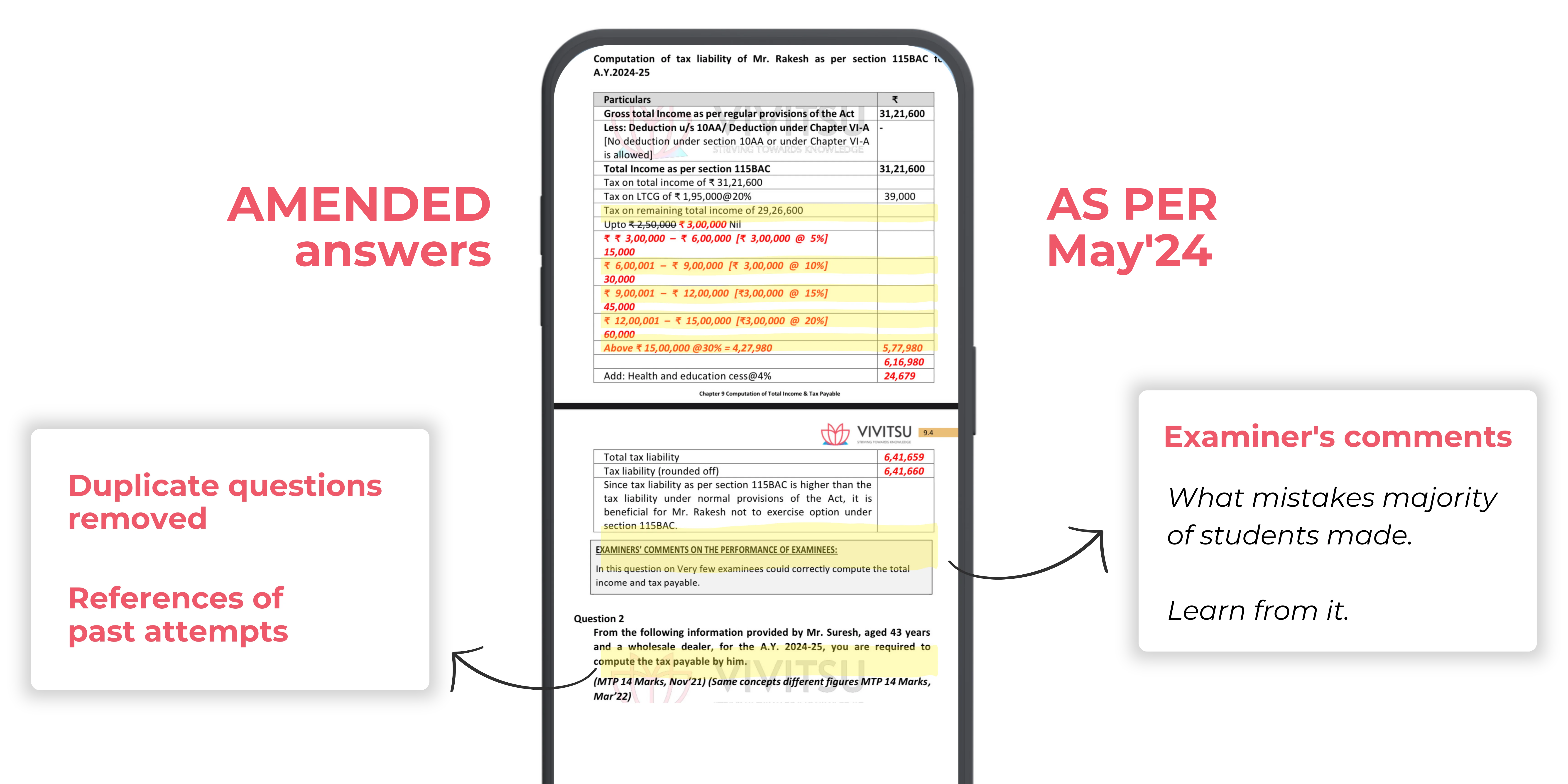

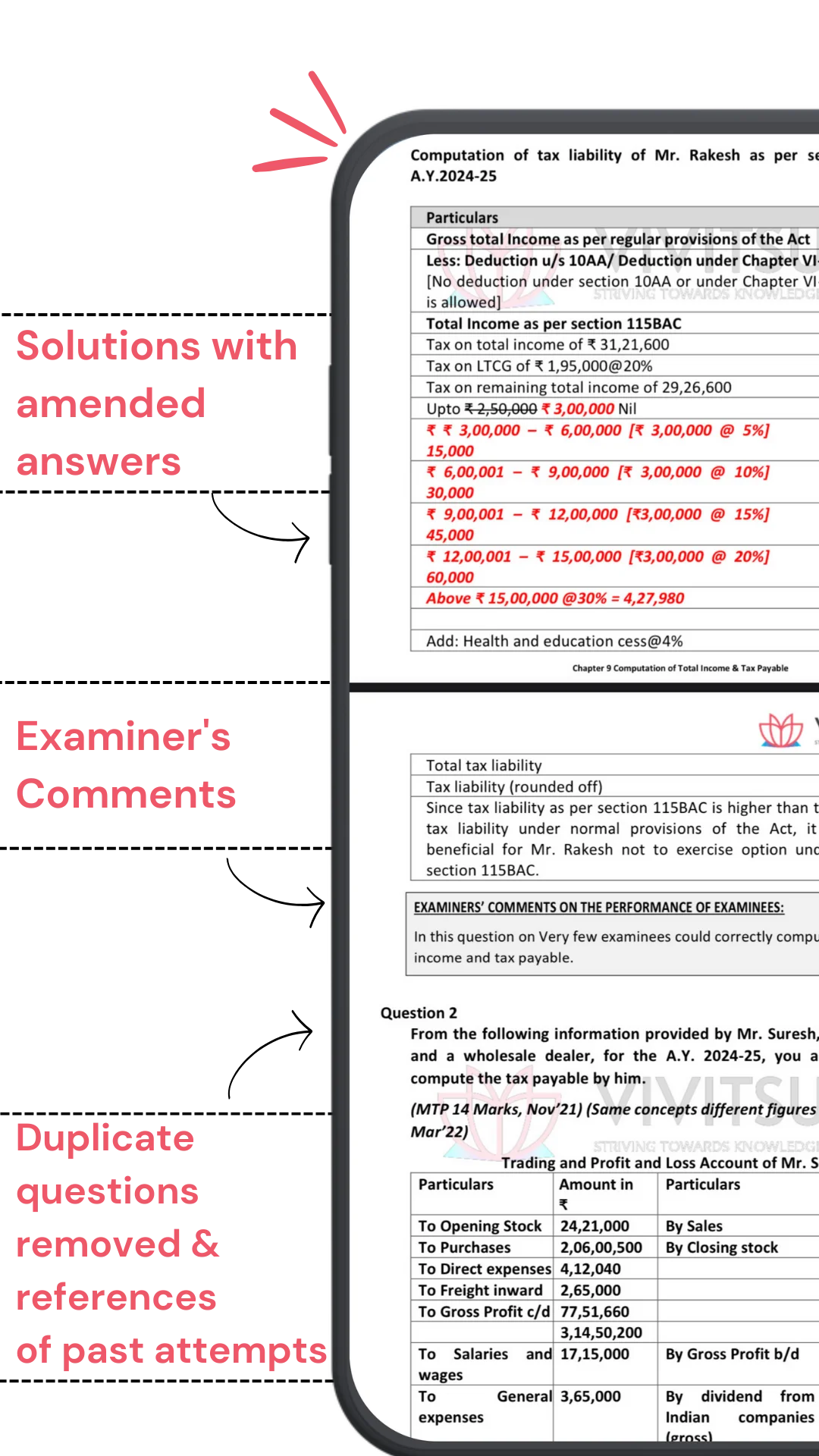

Amended answers

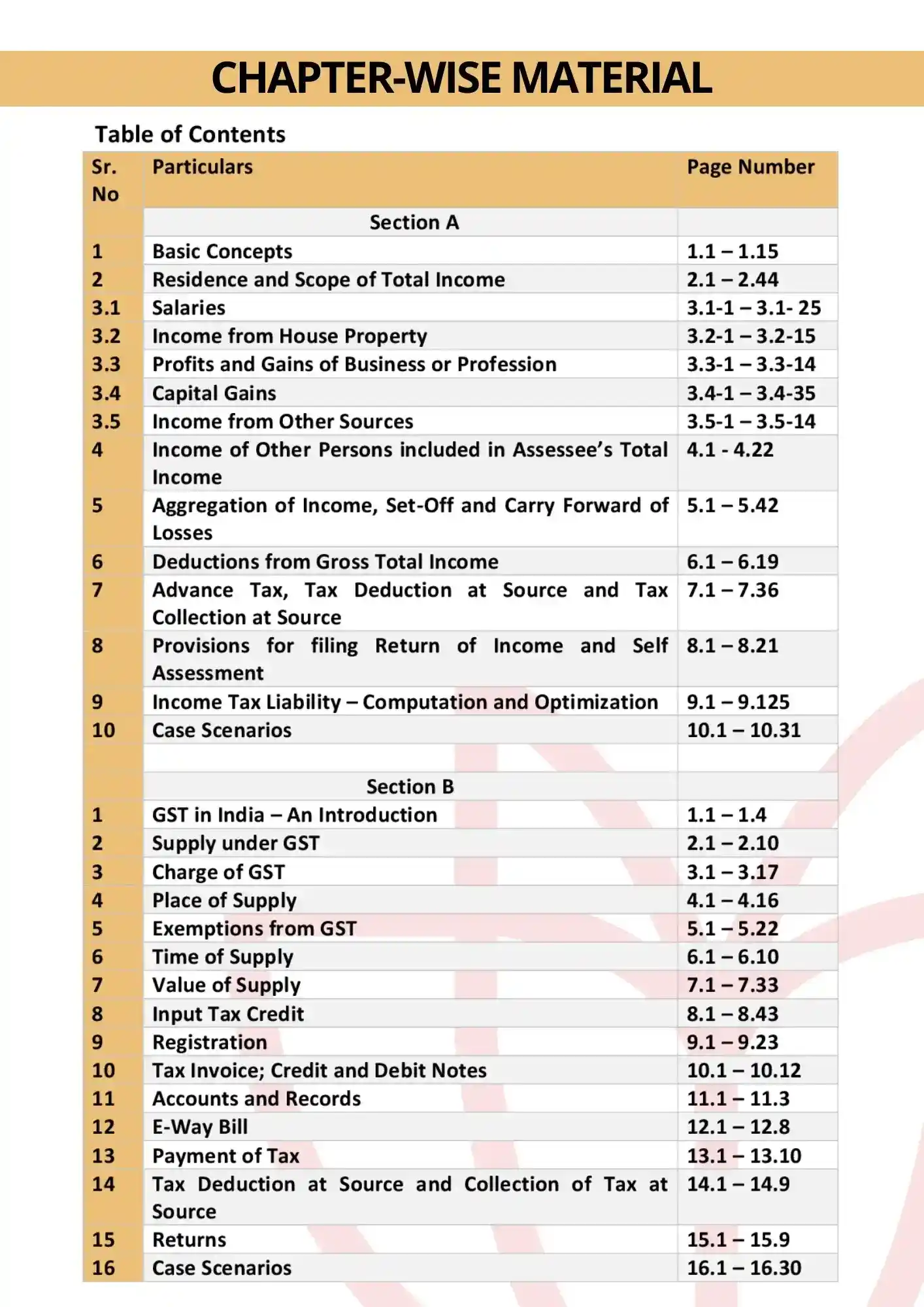

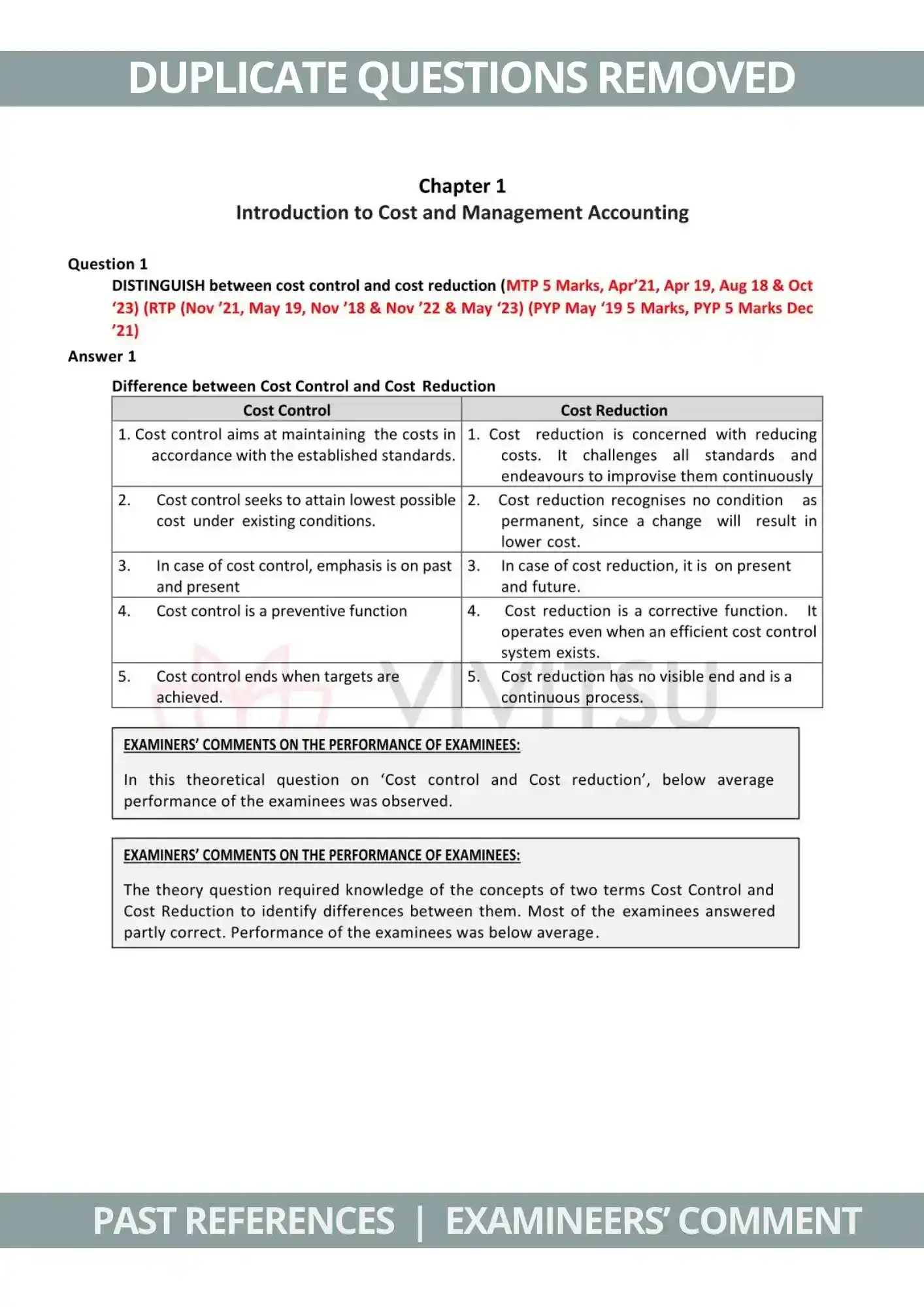

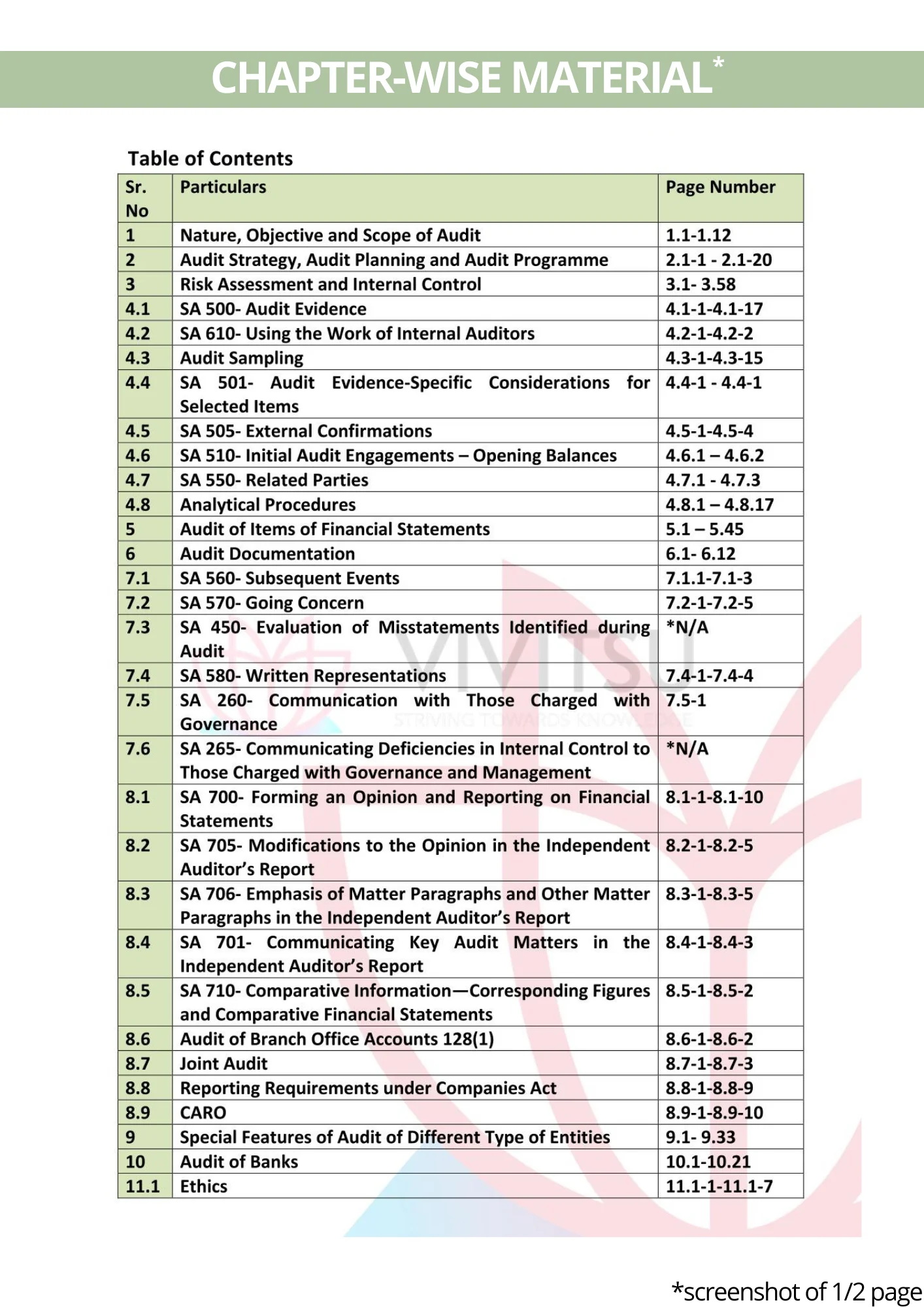

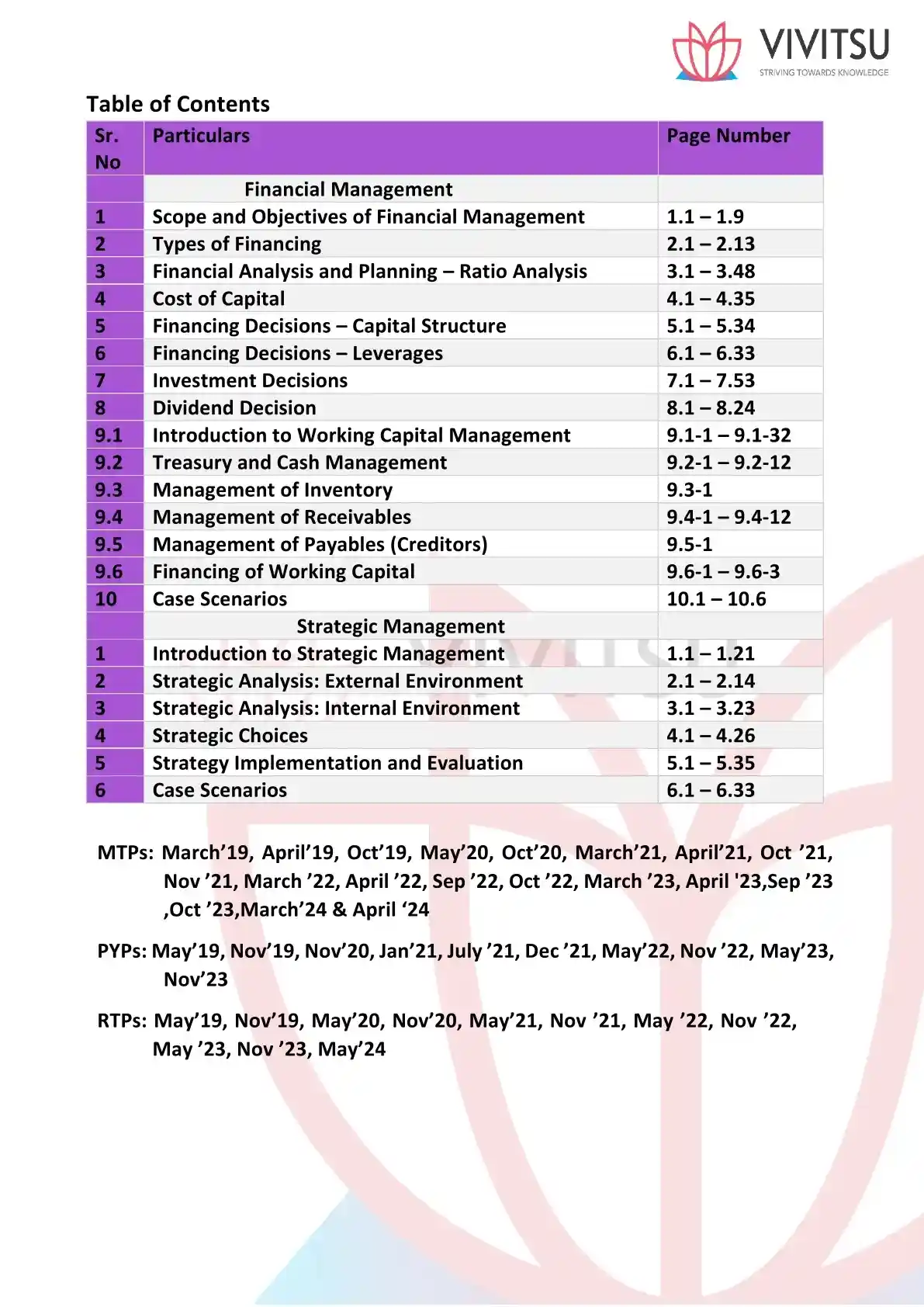

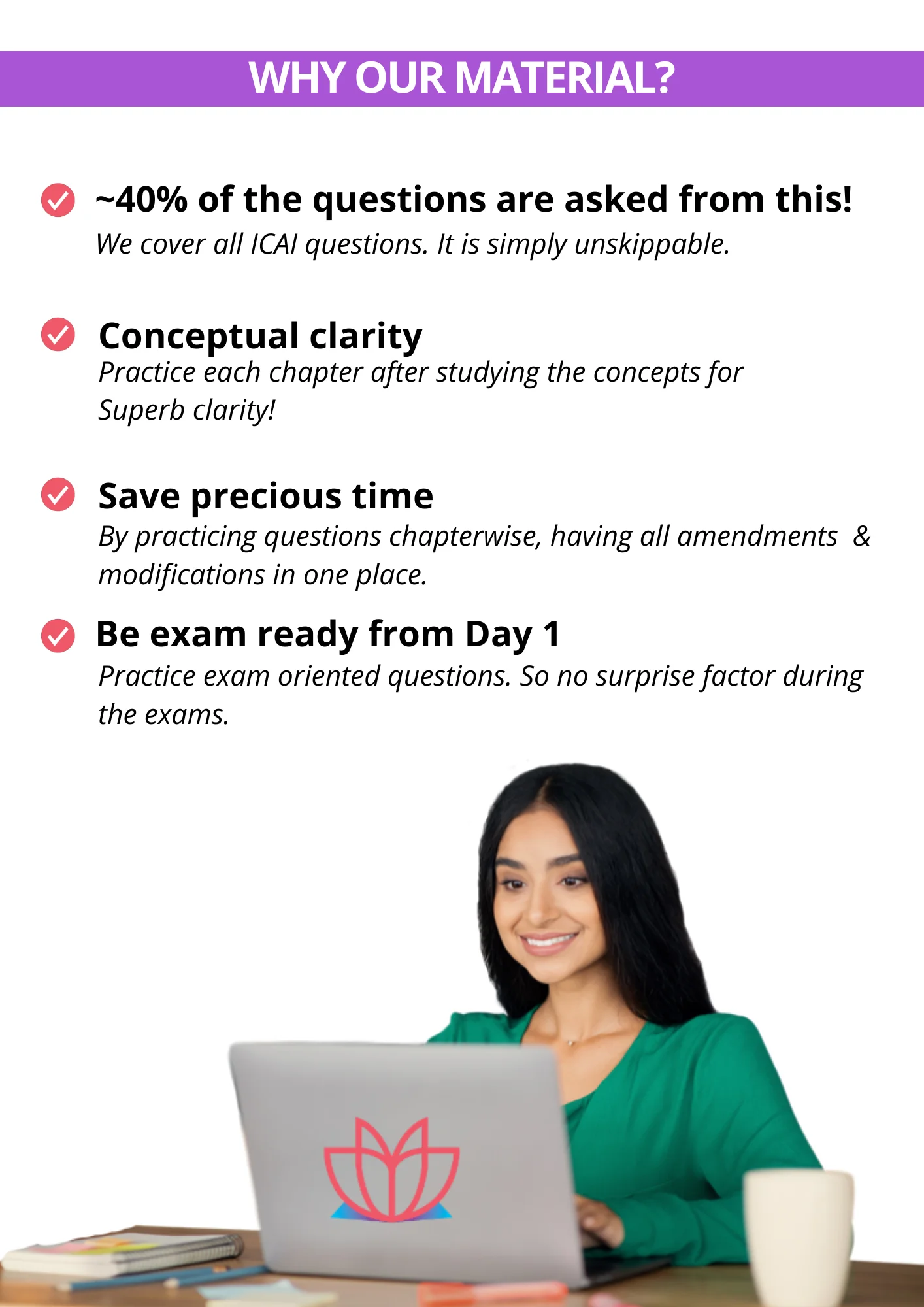

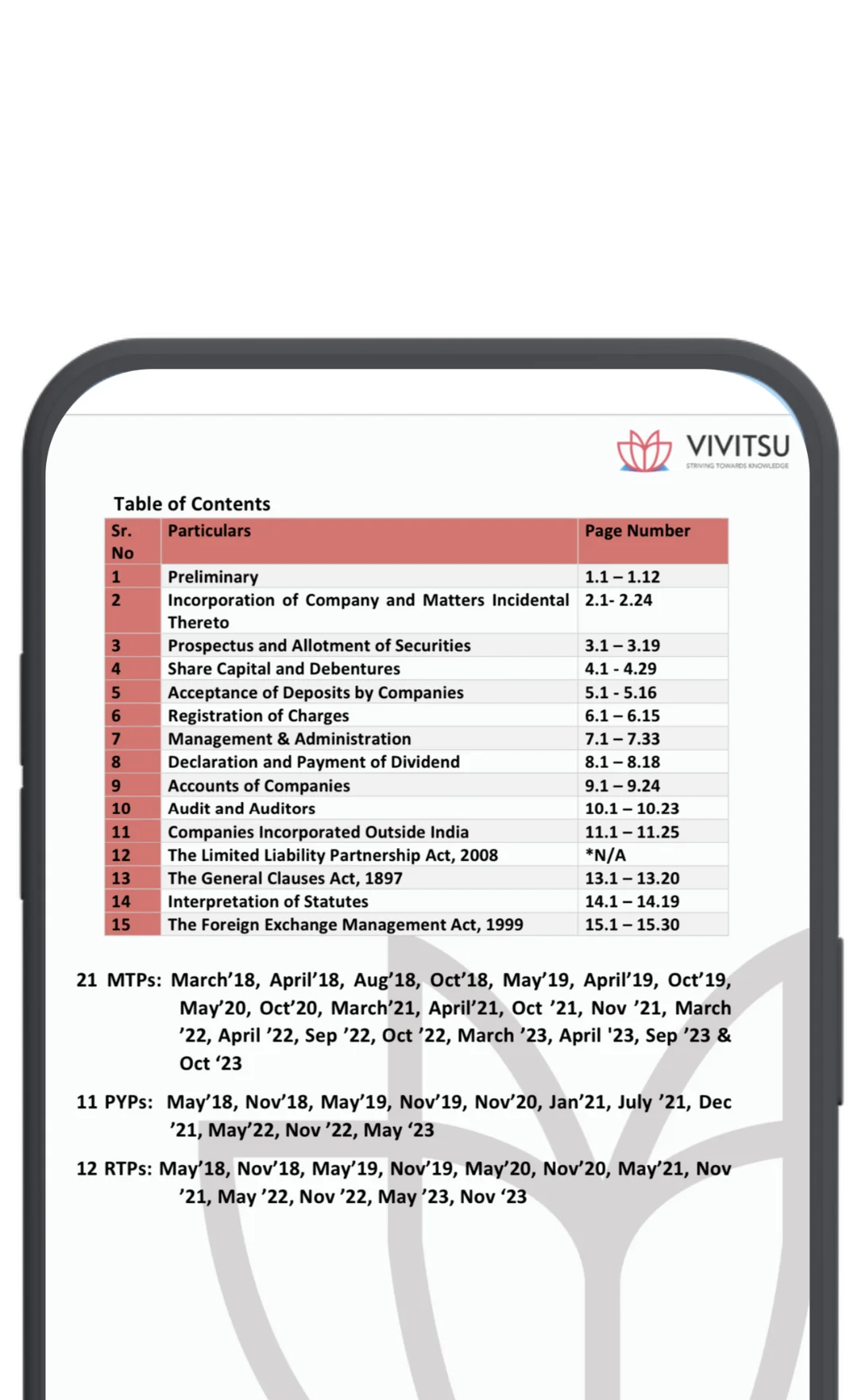

Chapter-wise compilation

Past References & Examiner comments